While cash management products are not directly related to credit cards, we thought that this was an interesting development in the personal finance industry and that our readers would be interested to read our assessment. Let us know in the comments below if you found this article useful and would like us to spend more time on non-credit card related articles such as these! Note: this is not a sponsored post and the review written is purely a reflection of the author’s views.

Edit: This post has been updated to reflect clarifications on projected returns and risk, provided after discussions with StashAway

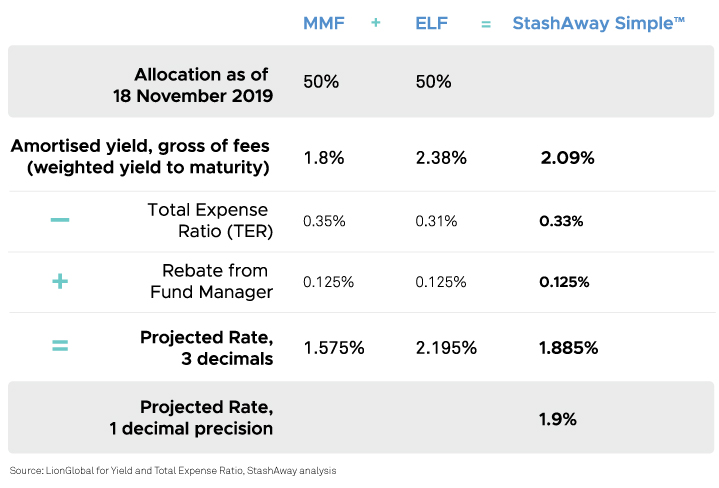

Today, I read an email about StashAway launching their a new cash management solution, StashAway Simple. Being curious, I took a few minutes to read about it, and wanted to share with readers my thoughts about it. StashAway Simple aims to deliver a projected net return of 1.9% p.a. to you with no minimum amount, no sales charge and can even accept SRS funds. This is done via investing in funds with an average expense ratio of ~0.33% p.a.; however StashAway will rebate 0.125% p.a., so your net expense ratio is 0.2% p.a.

All in all, this projected return is on par with some of the existing high interest rate savings accounts today (such as DBS Multiplier, StanChart e$aver, etc), but it is superior to these as investors would be able to obtain a higher interest rate without actually having to jump through so many hoops, such as crediting your salary or requiring you to make $500 monthly spend on your credit card. However, as with investing in all funds, there is some potential volatility of returns, and **you can actually make a loss **. As a potential customer reading about the launch of this new financial product, here are my quick thoughts:

What I like about StashAway Simple:

#1 No sales charge & no minimum balance

This is a big deal. If you were to invest your money into money market funds on Dollardex or Fundsupermart today, you would either be hit with a one-time sales charge (perhaps 0.5-2% of your investment amount) or an additional platform fee (perhaps 0.3% p.a. on your investment amount). These fees would seriously erode away your returns from investing your cash! I am thankful that StashAway’s solution is, in fact, going the opposite direction; instead of charging you fees, they are rebating management fees back to you  Moreover, they allow you to participate without a minimum balance, so it is really a great solution suitable for all savers (the ones with a few hundred dollars in your bank, as well as those who can save a few thousand dollars a month).

Moreover, they allow you to participate without a minimum balance, so it is really a great solution suitable for all savers (the ones with a few hundred dollars in your bank, as well as those who can save a few thousand dollars a month).

#2 No restriction on the duration required to take the money out

Simply put, this option makes StashAway’s cash management solution superior to fixed deposits (as one of the current alternatives to parking your liquid cash for a little bit of extra returns). With SGD 1 year fixed deposit rates ~1.8% p.a. today, this is a good, liquid solution to park your fund, and is in line with my expectations of a money market fund.

My concerns about StashAway Simple:

#1 Riskier than a pure money market funds

In an earlier version of this article, I accused StashAway of providing unrealistic projections. However, they have kindly provided the breakdown of how they projected a 1.9% p.a. return, which is based on:

- The amortized yield to maturity of the funds (According to this other article written by KPO and CZM, it is 50% exposure to a money market fund and 50% exposure to an enhanced liquidity fund)

- Plus: Rebates from Lion Global and StashAway

- Less: Total expense ratios of the funds

I find that this methodology is sensible, so technically it is possible to hit this projected returns today, assuming that the macroeconomic environment remains the same in the future. My apologies for the earlier accusation!

However, I do stand by my statement that the underlying Enhanced Liquidity Fund is not a money market fund. It is a short-term bond fund where you are actually taking duration risk [in an earlier post, I mentioned that you are taking credit risk; based on the “A” rating, it appears that they are ]. The duration of the Enhanced Liquidity Fund is 0.85 years whereas the Lion Global Money Market Fund has a duration of 0.25 years. How should you think about the Enhanced Liquidity Fund? As a reference point, the Enhanced Liquidity Fund will most likely give you a lower than that of Nikko AM Shenton Short Term Bond Fund, given that the Nikko AM Short-Term Bond Fund is riskier in terms of credit risk (credit rating of A- ) and duration (1.29 years).

Summary

This is an interesting new cash management product for Singapore-based savers. In today’s interest rate environment, it is technically possible to achieve ~1.9% p.a. assuming conditions remain in the status quo. However, if you are more risk-averse (as there is a chance that you could lose money even by investing in StashAway Simple), you could consider other relatively liquid products to give you ~1.5% p.a. interest, such as CIMB FastSaver account and Singapore Savings Bond, which have interest returns on your cash deposits guaranteed by the bank/government instead (a minimum $1,000 and $500 in deposits applies here).

If you would like to get the maximum rewards from your credit cards, do consider subscribing to our upcoming newsletter and follow us on Facebook to stay updated on the latest tips, tricks, and hacks to get the most out of your credit cards.

If you enjoyed this article, you may also be interested in:

- WhatCard’s list of best credit card sign up promotions

- WhatCard of the Week (WCOTW) 15 Nov: StanChart Unlimited Card

- WhatCard of the Week (WCOTW) 11 Oct: UOB One Card

- Best Credit Card Sign-Up Promotions to Earn Free Money

- Why do so many people continue to use their EZ-Link cards for MRT/Bus payments?

- You are throwing away money (and paying for my credit card rewards) if you use cash

- Get up to 10% cashback when paying for your taxes, utilities and insurance bills with this simple trick

- How I Got 72,000 Krisflyer Miles (worth $1,440) for Free!

and 1-year FDs were giving 1.5% to less than 2%. No wonder banks were pissed at upstarts offering higher yields!

and 1-year FDs were giving 1.5% to less than 2%. No wonder banks were pissed at upstarts offering higher yields!