Back in January 2020, DBS changed its terms and conditions for the DBS Multiplier account, a high interest savings account that is popular amongst many Singaporeans. The main change that affected many Singaporeans (including myself) is the disabling of the Singapore Savings Bond (SSB) ladder strategy, which previously allowed savers to be eligible under DBS Multiplier’s “salary credit + 2 categories” when they credited their salary (of >$2k/month) , charged $1 to their DBS credit cards and invested in SSB (previously considered as “investment” category)

We thought that this was an opportune moment to do our first introductory and comparison post on high interest savings accounts that are popular with Singaporeans today, based on realistic interest rates attainable (i.e. we would not suggest deliberately taking up an insurance policy with a bank just to earn an additional 1% interest for 12 months). And here it is!

What is a high interest savings account?

If you or your friends are currently using savings accounts such as the DBS Multiplier, OCBC 360, or UOB One you already know what high interest savings accounts are - they typically offer significantly higher interest rates of 2-3% per year as compared to a bank’s typical 0.05% p.a. base interest rate.

However in order to get these higher interest rates, the banks will require you fulfill other conditions such as crediting your monthly salary with the bank, spending on the bank issued credit cards, etc. High interest savings account are getting very popular these days because consumer always love higher interest rates, and banks use these as an opportunity to attract customer deposits and also build customer loyalty (i.e. make it harder for you to leave them) by tying you with multiple services across the bank.

What is the best high interest savings account for me?

At the risk of sounding like a broken record here, the best account depends very much on your personal life circumstances (just like the best combination of credit cards for yourself). However, we have found that the savings account that are popular with Singaporeans are generally tier their higher interest rates around similar categories, therefore we will do a comparison based on these categories:

- Monthly salary credit

- Credit card spending

- Giro/Bill payments

- Threshold of savings balance (i.e. if savings is >$25k, you will earn additional interest rate on savings above that and below $75k)

Methodology

We decided to compare the popular bank accounts in terms of effective interest rate (and the absolute dollar value of interest) against bank savings, spaced $5,000 apart from $10,000 to $75,000. This is done using the bank’s own calculators on their websites (in the case of BOC Smart$aver, there is a very helpful Google Sheets calculator). While there are many possible permutations available, we focused on the ones that probably apply towards more mainstream savers, and base it off the below monthly assumptions:

- Salary credit of at least $2,000

- Credit card spending of at least $500

- At least 3 GIRO/bill payments

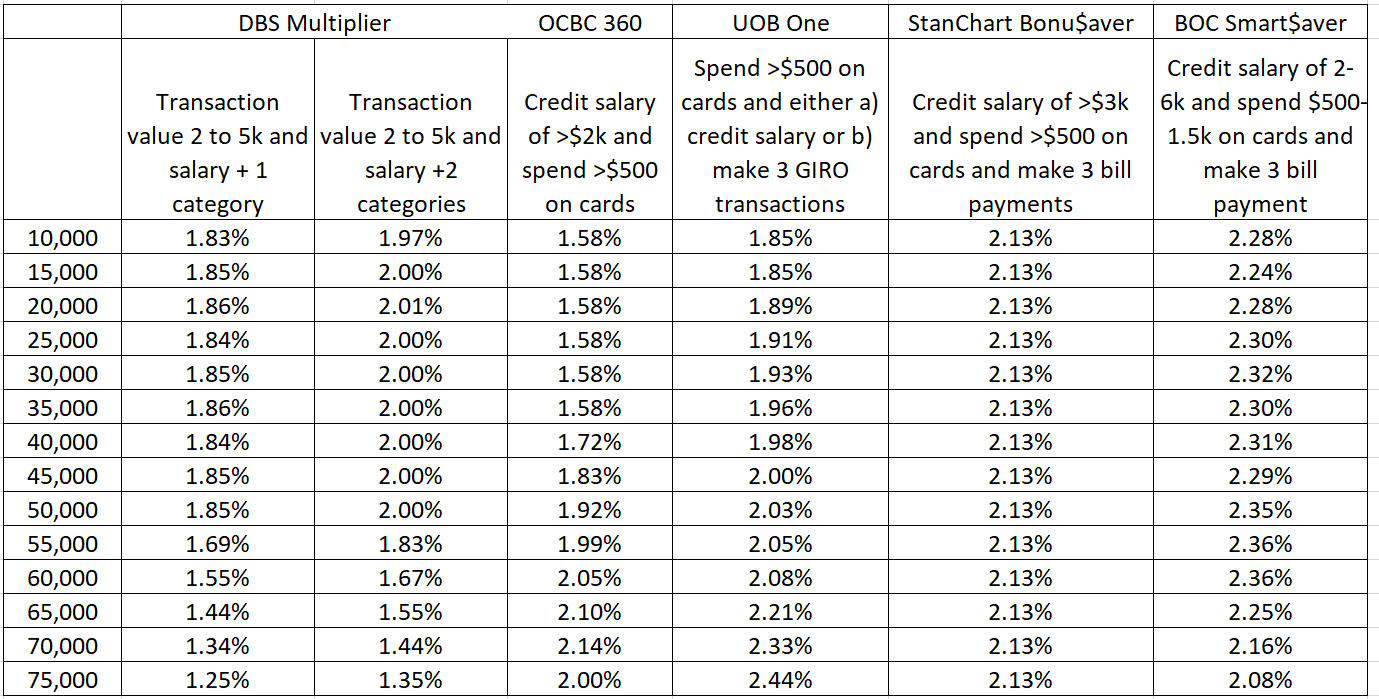

Here are our results based on these assumptions:

Effective Interest Rate Received

Summary

As you can see, even if you keep the conditions similar the savings accounts are most competitive at different amounts of savings. Based on the numbers above, we can make a few broad recommendations of what works best:

-

If you are planning to hold the full $75,000 (or more) in the account, go with UOB One Account. The 2.44% effective interest rate / $1827 is the highest in the comparison group, and this account also pairs really well with the excellent UOB One Card that is our top recommended cashback card for most people.

-

Otherwise, if you are willing to bear with BOC’s notoriously poor customer service experience, go with the BOC Smart$aver that offers the highest rates amongst all the other banks for amounts between $10,000-$70,000

-

If you prefer to have some actual customer service, the Standard Chartered Bonu$aver is the next best choice for you, offering a solid 2.13% interest rate regardless of how much you have in the account. Should you decide to get this account, do consider supporting WhatCard by applying for it via our affiliate link here.

Note: DBS Multiplier seems to be really uncompetitive in this comparison, but that is largely because we are assuming a “reasonable” total eligible transaction value of $2,500-$5,000 per month. Because of the way DBS Multiplier interest is structured, If you have able to increase your eligible transaction value through home loan payments, investments, or simply having a larger salary, the DBS Multiplier can give much higher interest rates.

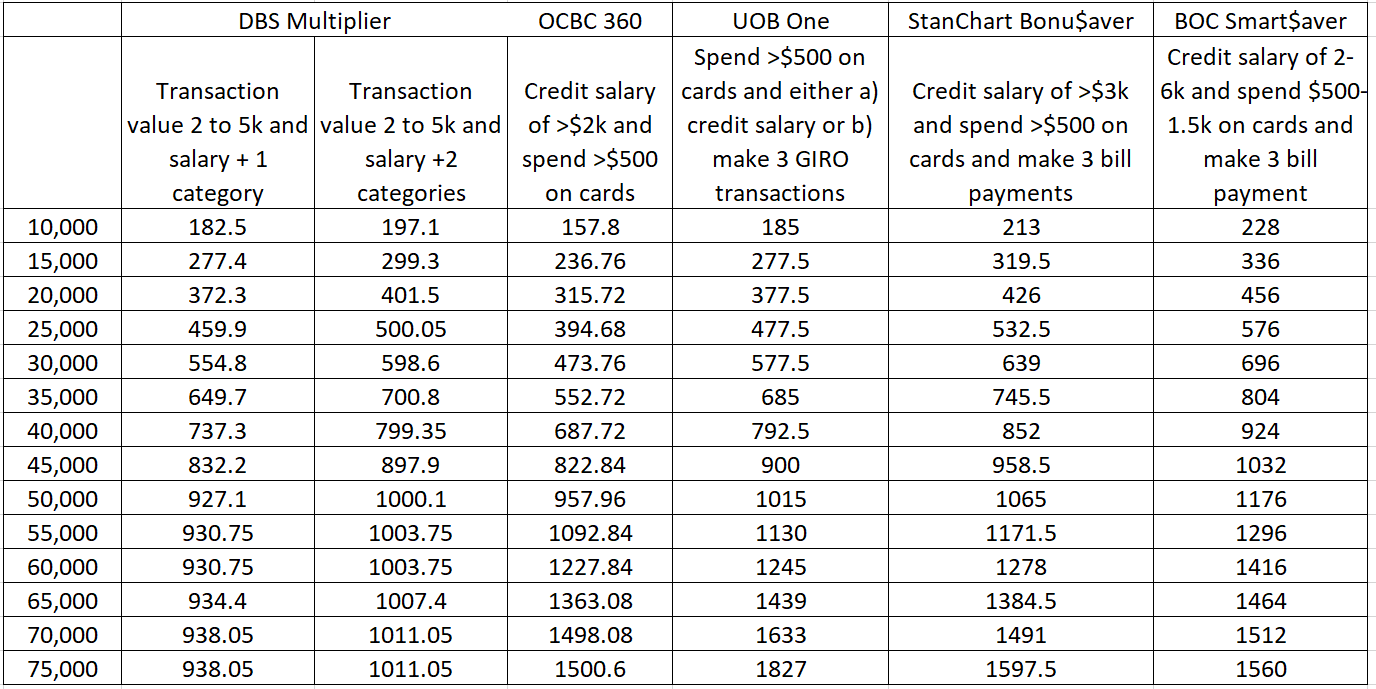

For reference, we are also including here the absolute dollar value of interest you will be getting with these different savings accounts:

Dollar Value of Interest Received

If you would like to get the maximum rewards from your credit cards, do consider subscribing to our upcoming newsletter and follow us on Facebook to stay updated on the latest tips, tricks, and hacks to get the most out of your credit cards.

If you enjoyed this article, you may also be interested in:

- WhatCard’s list of best credit card sign up promotions

- How much is a Krisflyer Mile worth?

- Does the MCO Visa Card live up to all its hype?

- A workaround for paying bills with GrabPay Credits

- Best cashback credit cards to use with SimplyGo for paying Bus/MRT fares

- Amex is excluding GrabPay topup from credit card rewards from March (except for Amex True Cashback)