NOTE: This is not a sponsored post. This article is part of an ongoing series of updates about the DBS Digi Portfolio. For those who are not up-to-date, you can read our earlier post here.

A month back, DBS announced that they were launching their own robo-advisory platform. I signed up as a beta tester in order to give readers of WhatCard a quick review of the tool.

Before diving into the review proper, I just wanted to share our “house”'s philosophy on robo-advisors; unlike other personal finance sites, we believe that the way to determine a top quality robo-advisors is not by the lowest platform / management fee charged to users, but by the robo-advised portfolio’s track record in re-balancing the portfolio. As many such robo-advisors have only sprung up in the past couple of years, few have a distinctively long track record. Hence, we try to pick out qualitative best practices when we can, and recommend our readers to pick the robo-advisors with the best process (as an initial proxy, until the track record can be determined). Finally, we want to highlight that generally, it is precisely in periods of large drawdowns in the capital markets that a retail investor panics and redeems, crystallizing the losses in his/her portfolio; thus, it may actually be more beneficial for such investors to consider having a personal financial advisor to manage their emotions and remain invested through the market cycle for long-run investment returns, since managing emotionsis precisely something that algorithms can’t do.

With that, I’ll begin, In full disclosure, the only other robo-advisor that I have invested with till date (purely as a personal experiment, and not via a deep analysis across all the robos) is StashAway. Hence, I will be reviewing what is available on the DBS Digi Portfolio VS StashAway.

Here’s what we like about DBS Digi Portfolio

1) Convenience & trust

The Digi Portfolio is ridiculously easy for you to invest your savings in. After logging into your internet banking, scrolling down on the main account page brings you to a button that takes you to a page where you can choose to invest in an Asian portfolio (to be funded in Singapore Dollars) or a Global portfolio (to be funded in U.S. Dollars). Choose your risk level, fill in some disclaimers and BAM! you are at the page where you can fund it with your savings or multi-currency account. In contrast, StashAway requires you to register your particulars to get started, and after completing the registration, you will need to follow instructions to do a wire transfer from your bank to their trust accounts. Therefore, administratively, StashAway is a higher friction robo-advisor.

Moreover, the whole time, you remain within the DBS internet banking infrastructure. So, you can trust that the same standards of care that the bank has (with you as a depositor) would be applied to the Digi Portfolio as well. On the other hand, robo-advisors like StashAway have to communicate trust with language on their website such as having an independent custodian (to allay concerns that in the event that they go bust, your funds will still be able to be recovered). My conclusion on the trustworthiness factor is: StashAway has a really good set-up to allay investors’ concerns, however there will always be a difference in the perceived trustworthiness/reliability compared to the bank that most Singaporeans grew up with.

It is so convenient to get invested in the Digi Portfolio

2) Historical returns analysis

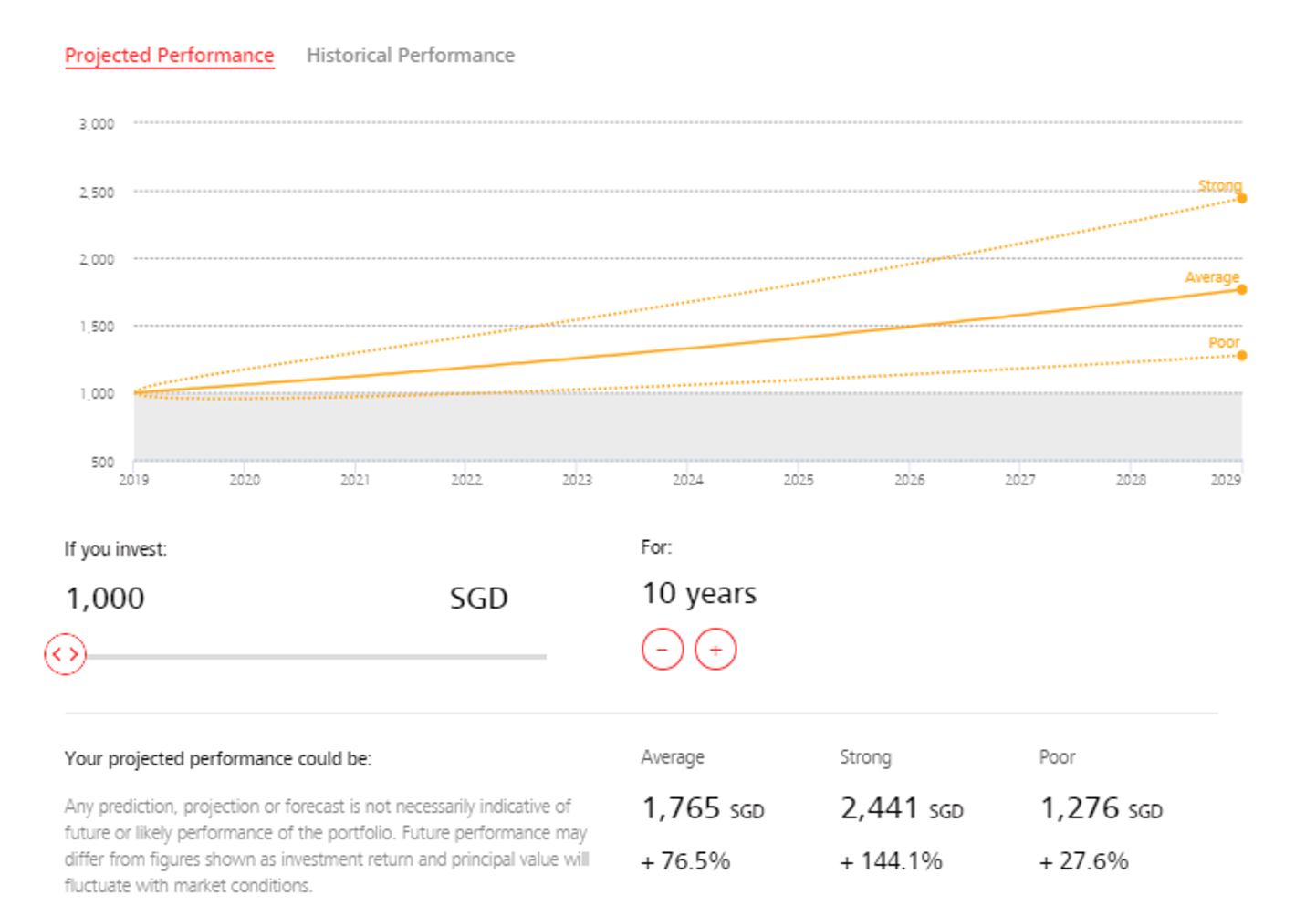

When you see total returns in a straight upwards trajectory over long periods of time, you should always be skeptical of the projections. More often than not, projected returns are used to “lure” people to invest in them, and the future rarely materializes as well as projected. The fund manager always caveats it with a fine print stating the past is not a predictor of the future. DBS is a culprit here; they similarly market their aggressive Asian portfolio as such:

However, I like the fact that they were also able to show the actual portfolio performance as well:

In my opinion, DBS launched their robo-advisory solution so late compared to their peers, in order to “seed” this fund and build an actual track record. This is the sort of processes that I like to see in robo-advisors; investing so with their own funds and the bank’s balance sheet, testing that it works before rolling it out to paying clients. When StashAway first launched, it was the first mover on a novelty concept, so many people back then (like myself) had to take a leap of faith to be invested in robo-advised portfolios. If you ask me, as the robo-advisory ecosystem is sufficiently mature today, it would be challenging for startup robo-advisors without a track record (like StashAway back then) to achieve significant traction in assets under management compared to the incumbents. Being one of the few that have a transparent track record available to investor gives the Digi Portfolio an edge over newer robo-advisors, but no particular edge over StashAway.

Limitations of DBS Digi Portfolio

1) Paying management fees on 5% cash allocation

Across all risk profiles, the Digi Portfolio has a standard 5% allocation to cash. In this hemisphere of positive interest rates, I wonder who would be happy paying fees on cash sitting in the portfolio? I don’t know what the allocation is like at other robo-advisors, but my impression is that robo-advisors substantially invest your funds, leaving only a small percentage of cash for liquidity purposes (managing subscription and redemption of funds)? In comparison, StashAway has a much more reasonable 1% cash allocation. I really hope that the DBS team reads this review and re-considers charging fees on such a high cash allocation. In an ideal world, fees should be charged for the portfolio assets excluding cash.

2) No considerations on risk

When you try to understand what you are invested in for the Digi Portfolio, you are directed to a link to download a factsheet. However, I found that the quality of exposure reporting in the Digi Portfolio is quite poor. Sure, they do tell you what ETFs they bought, but would you be able to know what is your effective exposure to China? How many percent of your bonds in the portfolio are high yield or investment grade? All these questions pertain to risks that you as the investor should know about, especially as Digi Portfolio may not the only investment product that you own. While also not the best risk reporter out there, I liked that StashAway gave me a breakdown of my exposure (and not just the names of the ETFs). It helps me understand how I should make allocation decisions on my other investment assets, based on the prevailing macroeconomic environment.

Our Summary

If you are getting started and have a healthy dose of skepticism of robo-advisors (as you rightfully should with all emerging technologies), I would encourage you to consider the DBS Digi Portfolio to start off with, judging by their initial attempts in doing the right thing for their customers. However, I do hope that the DBS team improves on the reporting of the portfolio exposure (the PDF fact sheets are quite useless for undestanding one’s risk when they are invested), as well as consider waiving management fees on cash in the portfolio, especially since it is a high 5% allocation.

If you have a considerable amount of savings, you may want to consider a small allocation (just to see how the DBS investment team allocates across the ETFs (the ETFs in Asian portfolio are: Nikko AM Singapore STI ETF, Xtracker MSCI China UCITS, Nikko AM Straits Trading Asia ex Japan REIT ETF, ABF Singapore Bond Index Fund, Nikko AM SGD Investment Grade Corporate Bond), and replicate the allocation yourself buying the same ETFs at brokerage firms. This would help you get the same portfolio but save more on the 0.75% management fees per annum, if you have the discipline to do so yourself and re-balance the portfolio periodically.

If you would like to get the maximum rewards from your credit cards, do consider subscribing to our upcoming newsletter and follow us on Facebook to stay updated on the latest tips, tricks, and hacks to get the most out of your credit cards.

If you enjoyed this article, you may also be interested in:

- WhatCard’s list of best credit card sign up promotions

- Get $200 in cash when applying for a Citibank card. New-to-bank customers only

- Best Credit Card Sign-Up Promotions to Earn Free Money

- Best credit card to top-up YouTrip : It’s (probably) not the card you are thinking of

- Why do so many people continue to use their EZ-Link cards for MRT/Bus payments?

- Video: Singapore Airlines Newark to Singapore (17.5 hours!) in Business Class

- Get up to 10% cashback when paying for your taxes, utilities and insurance bills with this simple trick