When you speak to any friends who use credit cards, it seems like everyone is in either one of two camps, either Team Cashback or the Team Miles, and each side will have reasons and arguments about why their chosen rewards is better

Quick Poll, which team do you belong to!

- Team Cashback!

- Team Miles!

- Still undecided …

0 voters

At a national level, many more Singaporeans use cashback cards as compared to miles cards. In fact, our own data shows that probably somewhere between 70-80% of all Singaporeans use primarily cashback cards - lets see if the poll results from above will validate these numbers!

Our experience is that many people get their first credit card without actually going through a proper comparison process. It could have been a friend’s recommendation, a sign up promotion you happened to stumble on, or in my case - OCBC sold me on the 365 Credit Card to pair with my OCBC 360 account that I was opening right after I graduated from university.

While people usually add more cards over time, what we also noticed is that people tend to stick to the same rewards type of their first card. Whether it’s was a cashback card or a miles card, they then continue on that same path without thinking through which one actually makes more sense.

We understand, cashback cards are generally much more popular because they are easier to understand and use. But how would you go about actually deciding which one would give you better value? Lets go over some of the major points of difference to help you decide which you should be choosing.

This is part of our Credit Card’s for Dummies series where we will be gradually developing a series of content to help people get started on optimizing their credit cards. For those who are just starting out, learn more about why you are “losing” money if you don’t use a credit card

Getting Cashback vs Airline Miles

The value of using a cashback card is clear – you are getting back value at whatever is the cashback rate. If you use the StanChart Unlimited Card that offers 1.5% cashback and spend $100, you are going to get back $1.50 of value. If you have a more optimized cashback strategy, you may be getting cashback of 3-5% on your UOB One Card, or maybe 5% using the DBS Live Fresh.

On the other hand, for miles cards you are instead getting Airline Miles with your spending, for example Citi PremierMiles 1.2 MPD (Mile Per Dollar spent), and DBS Womans World Card 4.0 MPD for all online spend.

Cashback is easy to understand and use the rewards (you just directly spend the cashback they credit to you), but for miles you have to use the miles to redeem a flight in order to realize its value - so if you had to compare miles vs cashback, how do you go about figuring out how much 1 mile on your credit card is worth?

The best value for your airline miles is to use it to redeem a premium flight experience (Business/First Class) that you would normally never pay cash for.

This is a long and complex topic and we have written a separate much more detailed article for those interested in reading more about it, for those who just want the short answer: in general a mile is worth anywhere around 1.5-2.0 cents - for the purpose of this article’s comparisons we will take the middle point and assume a mile is worth 1.75 cents.

Cashback vs Miles Rewards

To figure out how much rewards you can actually get using either cashback or miles cards, we have listed below some common popular options for each, as well as the highest rewards rate you can get from them assuming you optimize your spend on them perfectly - in reality you will probably get a somewhat lower rate than what is listed below:

| Cashback Card | Cashback Rate Up To |

|---|---|

| UOB One | 5.0% |

| DBS Live Fresh | 5.0% |

| OCBC 365 | 6.0% |

| StanChart Unlimited | 1.5% |

| Amex True Cashback | 1.5% |

| Miles Card | Miles Rate Up To | Miles Value (at 1.75 cents per mile) |

|---|---|---|

| Citi Rewards | 4.0 | 7.0% |

| DBS Womans World | 4.0 | 7.0% |

| Maybank Horizon | 3.2 | 5.6% |

| Citi PremierMiles | 1.2 | 2.1% |

| Amex Krisflyer | 1.1 | 1.9% |

As you can see the difference in value might not seem very significant, however we will argue that for Miles cards you will likely get higher value because it is much easier to get the top miles earning rate of 4.0 MPD as opposed to for Cashback cards, which often requires a lot of optimization to get the promised 5-6% cashback as these cards often have minimum monthly spending to get bonus cashback AND a low cashback cap that limits how much value you can actually get.

If you are good at optimizing your cashback strategy, you can often get as much as value as miles cards, but this is not easy to achieve and often depends heavily on what your current spending pattern is. In general, a miles approach will return a higher value than a cashback one.

Optimizing for Cashback vs Miles Rewards

Besides awarding different types of rewards, cashback and miles cards also differ quite significantly in terms of how you actually optimize your rewards from the cards, that can affect your choice of strategy. As a general guide:

-

Cashback cards favour having a single card to cover multiple different expense categories (e.g. eating out, shopping, online spend).

-

Miles cards favour having different cards for different expense categories.

We will go through optimizing for each of these in more detail:

1. Optimizing for a Cashback strategy

For cashback cards, you tend to get the highest rewards using cards that have a significant monthly minimum spend, and (often) various cashback categories that you have to spend on in order to maximize your rewards.

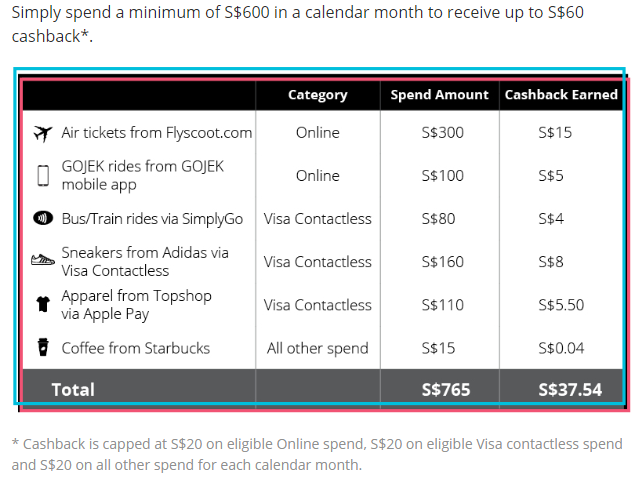

For example, the DBS Live Fresh card advertises an attractive 5% cashback rate applicable to two major spending categories: Visa Contactless (aka PayWave) and Online spend. However, to qualify for the 5% cashback you have to hit a minimum monthly spend of $600, and this 5% cashback is capped at $20 for each of the two categories. Any other spending gets you a palty 0.3% cashback.

Example of rewards from the DBS Live Fresh Card from the DBS website

Hence, in order to maximize your cashback rewards from the DBS Live Fresh card you have to spend at least $600 per month on the card, evenly split between the two different categories to avoid hitting the $20 category cashback cap.

In general, Cashback cards are suitable for those who:

- have consistent monthly spending on daily household spending such as dining out, groceries, and petrol

- prefer to own and manage a fewer number of cards

- do not travel very often

2. Optimizing for a Miles strategy

On the other hand, miles cards typically have no minimum monthly spend, and many having no rewards cap as well. This makes them more suitable for those with less regular spending (not much regular daily spending, but occasional large purchases such as air tickets/online purchases). The basic miles cards such as DBS Altitude, Citi PremierMiles, OCBC 90N also tend to come with bonus rewards for travel spending and free airport lounge access that make them ideal for those who travel regularly.

However, as many miles cards tend to give bonus rewards for just 1-2 specific spending categories, an optimal miles card strategy will usually involve holding at least 2-3 different cards, each tailored for a specific spend. For example:

- the DBS Womans World Card gives 4.0MPD for all online spend and 0.4 MPD otherwise

- the Citi Rewards Visa gives 4.0MPD across many retail/shopping, ride hailing, and other merchants, but 0.4 MPD for all others

Both of these cards have no minimum monthly spend.

Because the rewards cap for miles cards are also usually much higher than for cashback cards, miles cards are usually better for those who spend larger amounts each month (>$2,000/month) that would cause you to run up against rewards caps for cashback cards.

In general, Miles cards are suitable for those who:

- have less consistent, but higher average monthly spending,

- willing to own and manage multiple cards

- willing to spend more time and effort optimizing rewards as well as miles redemption value

- travel regularly - especially if you have dreams to use your miles for the chance to travel on premium cabins (e.g. First/Business Class)

Summary

There is no clear-cut answer to whether you should use cashback or miles cards because it varies significantly based on personal lifestyle and preferences, but we hope that by sharing these information we can help you to make a better informed choice about which approach you should be following – and not just decide based on which you feel more comfortable with!

If you would like us (or others) to help you figure out if your current credit card strategy make sense, post on our forum and let the WhatCard community help you out!

If you would like to get the maximum rewards from your credit cards, do consider integrating WhatCard into your lifestyle to help you optimize your credit card rewards, and follow us on Facebook to stay updated on the latest tips, tricks, and hacks (like this article!) to get the most out of your credit cards

If you enjoyed this article, you may also be interested in:

- This is how you set up ipaymy to reduce your IRAS tax payments

- WhatCard's list of best credit card sign up promotions

- Best credit card to top-up YouTrip : It’s (probably) not the card you are thinking of

- Why do so many people continue to use their EZ-Link cards for MRT/Bus payments?

- Video: Singapore Airlines Newark to Singapore (17.5 hours!) in Business Class

- Get up to 10% cashback when paying for your taxes, utilities and insurance bills with this simple trick

- The (plastic) X Card is back, with a 60,000 miles sign up promotion